In February 2026, scholars from several disciplines gathered at the University of Lucerne to discuss digital payment infrastructures, data, and the future of money.

Bringing Payment Research Together

From February 4–6, 2026, we hosted the workshop “Platforming Digital Payments: Infrastructures, Data Assets, and Future Imaginaries” at the University of Lucerne. The event marked the closing phase of our SNSF research project Digital Payments – Making Payments Personal and Social.

The workshop brought together scholars researching digital payments from a variety of perspectives, including sociology, media and communication studies, political science, economics, and history. Together, we explored how digital payment systems are reshaping economic infrastructures, social relations, and everyday financial practices.

Discussing New Research on Payment Infrastructures

The workshop was organized around the discussion of pre-circulated paper drafts. This format allowed participants to engage deeply with each other’s work and to provide detailed feedback.

The papers addressed topics such as the platformization of payment infrastructures, the role of transaction data, the relationship between payment systems and consumption, and the imaginaries shaping the future of money. The discussions highlighted how payment technologies increasingly function as socio-technical infrastructures that organize markets, generate data, and influence economic behavior.

Building a Research Network on Digital Payments

Beyond the paper discussions, the workshop provided an opportunity to strengthen connections within the growing international research community studying payments and payment infrastructures.

The lively discussions and informal exchanges confirmed the importance of building a network across disciplines to better understand how digital payments are transforming economic life. We are grateful to all participants for their stimulating contributions and for helping to make the workshop such a productive and inspiring event.

The field of payment technologies is evolving rapidly. Over the past decade, digital innovation has driven a diversification of payment solutions. Today, we see a wide range of technologies: payment apps for in-store and peer-to-peer transactions, mobile platforms issuing special monies (Zelizer, 2011), and money-like tokens such as airtime credits, loyalty points, gift vouchers, in-game currencies, and even customer data (O’Dwyer, 2023). These developments have introduced new actors and infrastructures, creating a digital payment economy (Elder-Vass, 2016) that fuels innovative business models, products, and services.

From Fees to Data: A Shift in Business Models

This transformation is not limited to how we pay. The entire payment ecosystem has shifted from fee-based models to marketing-driven approaches, where transaction data is monetized (Maurer and Swartz, 2017; Swartz, 2020). These changes reshape relationships and dynamics within the networks that underpin everyday payments.

A Sub-Project on the Digital Economy of Payments

In a sub-project we examine how the practices and mechanisms of the digital economy are translated into payment technologies and embedded in socio-technical infrastructures. Insights from economic sociology, the anthropology of money, and digital marketing show how payments and transaction data are used to observe individuals, integrate them into systems, and shape relationships (Coll, 2013; Mützel, 2024; Zelizer, 2011). Studies on the data economy explain how data is monetized and infrastructures are built (Fourcade and Kluttz, 2020; Lauer, 2017; Mellet and Beauvisage, 2019). Combined with Science and Technology Studies (STS), these perspectives reveal how payment infrastructures merge social and technical elements to enable, shape, or transform relationships (Bowker and Star, 1999; Latour, 2005; Helmond, 2015; Tkacz, 2019).

This project contributes to understanding how technological innovation and shifting expertise create new relationships and markets. Proposed is an analytical framework for socio-technical change, illustrated through payment systems. It identifies three phases: anticipation, negotiation, and institutionalization. The anticipation of a data-driven future and marketing concepts guiding actors performatively shape subsequent developments.

The observation of the payment systems field concludes in 2025 and looks ahead: under the imperatives of data and extraction, payment data has become a valuable resource, monetized on virtual markets for personalized advertising.

Further Reading

Bowker, G., Star, S. (1999). Sorting things out. Classification and its consequences. Cambridge. MIT Press.

Callon, M. (1998). The laws of the markets. Blackwell.

Elder-Vass, D. (2016). Profit and gift in the digital economy. Cambridge University Press.

Fourcade, M. & Kluttz, D. N. (2020). A Maussian bargain: Accumulation by gift in the digital economy. Big Data & Society, 7 (1), 1–16.

Kjellberg, H., Hagberg, J., & Cochoy, F. (2019). Thinking market infrastructure: Barcode scanning in the us grocery retail sector, 1967–2010. In M. Kornberger, G. C. Bowker, J. Elyachar, A. Mennicken, P. Miller, J. R. Nucho, & N. Pollock (Eds.), Thinking infrastructures (pp. 207–232). Emerald Publishing Limited.

Maurer, B. (2012). Payment: Forms and Functions of Value Transfer in Contemporary Society. The Cambridge Journal of Anthropology, 30 (2), 15–35.

Mellet, K. & Beauvisage, T. (2019). Cookie monsters. Anatomy of a digital market infrastructure. Consumption Markets & Culture, 23 (2), 1-20.

Swartz, L. (2020). New Money: How Payment Became Social Media. Yale. University Press.

Zelizer, V. A. (2011). Economic lives: How culture shapes the economy. Princeton University Press.

When we think of platforms, we think of them as something new. This makes sense, as platforms have become the business model to emulate: Many of the most successful companies are platforms or operate platforms. Think of Amazon’s e-commerce and cloud platform, Apple’s app store, or Google’s advertising business.

However, these companies did not invent the platform model. Platforms, especially in payment, have a long history, though they were not called platforms at the time. Let me give you an example.

AKO Bank

In the 1930s, specialized Swiss credit banks launched aggressive campaigns to lend to consumers. AKO-Bank, also known as »Angestellten Kredit Organisation« or »Anspar- und Kredit Organisation«, was one such bank. The system operated according to the »French method«.1 Creditworthy individuals received paper tokens that they could use like cash in participating shops.2 Debts had to be paid back with interest (typically 18 percent annually) after six months. Sellers were guaranteed payment, but only after the six-month repayment period had passed. This »French method« consumer credit antecedes the introduction of the first »universal» credit card by Diners Club in the 1950s. Basically, the AKO bank issued its own credit-based currency and recruited merchants willing to accept it while paying a commission for the additional business coming their way—similar to the early credit cards.

Before consumer credit banks succeeded in Switzerland, consumer credit was left mainly to retailers and department stores (see Saxer 1978). Due to insufficient means to gauge customers‘ creditworthiness, it was derogatorily called »wild credit«. Normal banks only became interested in consumer credit in the late 1960s.

AKO Bank as platform?

AKO Bank’s business model exhibits all the factors of platformisation: They set up a data infrastructure to quickly gauge customers‘ creditworthiness.3 They established a two-sided market with merchants desiring additional business on the one side and debtors wishing to buy a wide range of goods and services at cash prices. And they governed the interactions between these two sides (and the wider public) by matching the needs of the salaried class with a morally adequate range of merchants and goods to buy on credit.

A Data Infrastructure to Gauge Creditworthiness

To receive credit from AKO Bank, hopefuls had to fill in a questionnaire with 29 questions concerning their financial standing: information about employer, income, living arrangements, expenses, etc., served to calculate the possibility of monthly credit repayment. Director Walter Rentsch explained their rating of creditworthiness: An average Swiss household could spend 15 percent of its monthly income on unplanned expenditures. To be on the safe side, the allowable payback rates must not be higher than 7 percent of monthly income. With all the data provided by the hopeful debtors, the credit clerk should decide on the same day the hopeful borrower lodged their application.

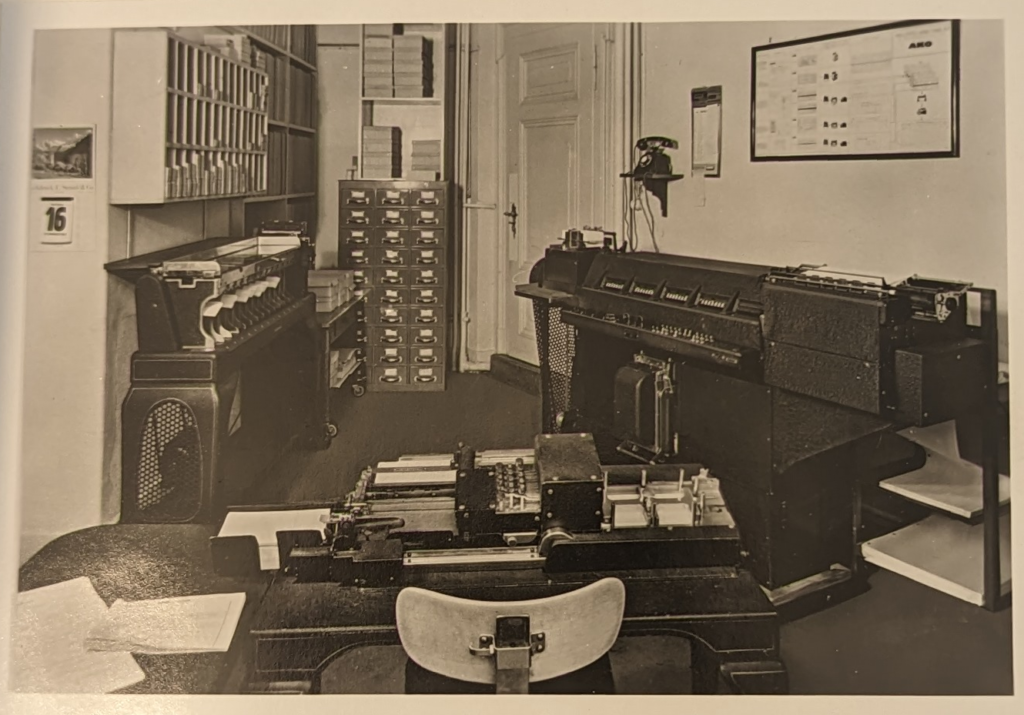

In the 1950s, the bank boasted a state-of-the-art Hollerith punchcard database to handle its customers‘ information about monthly rates due or late fees (see Figure 1 below). This »mechanization of accounts« was also part of a carefully constructed public image.4 (see also Carruthers/Espeland 1991). As is evident from the AKO’s marketing materials of the time, it emphasized the rationality of its operations—not »wild credit« but well-organized credit—and the economic common sense of using credit for certain purchases.

Figure 1: AKO Bank’s Hollerith Punch Card Database in its Zürich office (around mid 1940s).

The AKO Bank defined itself against the prevailing business of installment credit provided by retailers and department stores. As they wrote in their marketing materials, the goal of this »wild« and unordered practice was to increase sales on the back of over-indebted consumers woefully neglecting their individual financial circumstances. Not so at AKO Bank! They claimed to only give credit to creditworthy individuals. As a proof, they boasted a one-percentage point default rate. While they had a high yearly interest rate of about 18 percent, their business model allowed them to subsidize the debtors. At the time, lending directly to consumers had quite a large overhead as AKO sometimes argued to justify its interest and servicing fees (for debtors) and commission (for merchants).

AKO’s Payment Architecture

To better understand the business model of AKO, we must shift our focus from credit to payment. If we look at credit, we see only the debtors without the other part of the equation. Creditworthy individuals received the sum neither in giro-money nor in cash: They got a paper token that only participating merchants could redeem. In fact, AKO issued a kind of special money—»AKO-Bons« (see figure 2 below). Only AKO-approved merchants could accept this money and redeem Swiss francs when they returned it to AKO.

Figure 2: AKO Bon from 1943.

From a business perspective, AKO positioned itself as a payment intermediary between creditworthy buyers and participating sellers—much like the three-party credit card systems Diners Club or American Express that emerged in the 1950s and 60s. This intermediary position allowed AKO to profit from both sides‘ participation: the debtors paid interest, and the merchants paid a commission of 10 percent to have access to AKO customers, supposedly bringing in additional business.

To gain customers, AKO heavily advertised in newspapers. To recruit merchants, they offered a broschure boasting a »scientifically neutral depiction of the effects of participation in our organization«. A lecturer from the business school in St. Gallen calculated how much merchants could profit from participation: additional business from AKO customers, guaranteed payment even in case of default, not needing their own credit department, etc. These must have been real advantages to merchants, as the numerous participating merchants published in full-page advertisements suggest. Of course, these advertisements also must have had the function of putting FOMO into merchants—comparable to the introduction of credit cards in Switzerland when non-accepting hotels feared a loss of customers who wished to pay with a card.

Governing Relations Between Borrowers, Merchants, and Platform

As we have seen in research on digital platforms, the platforms govern relations and interactions between users and complementers (e.g., passengers and drivers in Uber’s case). AKO governed the relations between debtors (users) and merchants (complementors) in three ways: Firstly, when paying AKO, customers must hand over their AKO bons. As such, they marked their difference as non-cash-paying customers. This was a cause for anxiety: sometimes AKO customers didn’t buy in their hometowns, where they were well-known, even though they had participating AKO merchants. Also, credit customers sometimes paid higher prices (although not with AKO, as they promised).5 Secondly, AKO designated the salaried class as its primary customer base. This category of customers was located between lowly workers and aspired to be more bourgeois/middle class.6 They were a bit more economically secure than workers,7 but couldn’t afford the aspired lifestyle — hence credit.

Thirdly, AKO, its customers, and merchants had to navigate the fraught morality of consumer credit. For the salaried class, it was necessary to keep up appearances (see Kracauer 1998 below), but to the general public, it seemed frivolous to get a haircut on credit as it was discussed in NZZ.8 AKO had some control over this matching of customer base and morally adequate merchants. Still, it was evidently a tightrope walk as AKO periodically had to publish advertisements declaring that AKO-bons could not be used to buy luxury goods (see figure 3 below).

Figure 3: »You can’t buy luxury items with AKO-Bons«.

As we have seen, the AKO bank platformised consumer credit by handing its own cash-like currency to creditworthy customers to spend at participating merchants. Fifty years of successful operation attest that it successfully re-intermediated retailers and department stores as main issuers of consumer credit.9

What do we gain when we use a platformization lens to examine payment? We should gain a clearer sense of what is new about digital platforms: how they turn data into power. However, we should also see what remains the same: platforms governing relations between themselves, users, and complementors—with or without data.

Saxer L (1978) Das Schweizerische Konsumkreditgeschäft: sozialpolitische Aspekte der bankmässigen Konsumkreditgewährung. Bankwirtschaftliche Forschungen 50. Bern: P. Haupt. ↩︎

The French method differs from the »American method«, where banks assisted sellers in entering into credit relations with buyers to buy certain high-cost items like cars. Merchants were responsible for advertising, contractual relations, and risk. ↩︎

Neue Zürcher Zeitung, Den Daumen oder den Franken…? July 4, 1938. ↩︎

From 1934, it operated as an independent credit bank. In 1968, it was taken over by SBG (today’s UBS). In 1991, it merged with Bank ORCA, another consumer credit subsidiary of UBS, and its brand identity was discontinued. ↩︎